IRS FORM 8949 & SCHEDULE D

A COMPREHENSIVE GUIDE FOR TRADERS & ACTIVE INVESTORS

IRS FORM 8949 & SCHEDULE D

A COMPREHENSIVE GUIDE FOR TRADERS & ACTIVE INVESTORS

Most traders and active investors reporting capital gains and losses must file Schedule D and Form 8949 with their tax return. These forms have an ominous reputation for the complexity involved. This guide is your resource to comprehend calculating cost basis and adjusting wash sales, correctly reporting short sales, and understanding the various form categories and layout.

CONTENTS

IRS Schedule D:

IRS Form 8949:

IRS SCHEDULE D EXPLAINED

IRS Schedule D is the tax form where traders and investors file capital gains and losses from trading or investment activity. Individual trade details are recorded on IRS Form 8949, and the totals from this form flow to the Schedule D. Other capital gains/losses may also be reported on Schedule D, but the scope of this guide is focused on trading.

The following securities are reported on Form 8949:

- Stocks

- Bonds

- Warrants

- Options

- DRIPs

- Mutual funds

- Single-stock futures

- Exchange traded funds / notes (ETFs/ETNs)

Some securities are classified as Section 1256 contracts. These securities are reported on IRS Form 6781 with totals flowing onto IRS Schedule D.

These securities are reported on Form 6781:

- Futures

- Exchange traded / broad-based index options

Those who have elected IRS Section 475f Trader Tax Status and use the mark-to-market accounting method will record their qualified trade activity on IRS Form 4797 – Sales of Business Property. However, trades that are segregated as investments would still be reported on Schedule D. Most brokers do not provide a Schedule D or Form 8949 to clients, and they’re not required to by the IRS. The fact is: your broker usually cannot provide a complete Schedule D or Form 8949 report. The IRS has always held taxpayers responsible for producing accurate Schedule D reporting. The Schedule D is used with most tax returns – 1040, 1041, 1065, 1120 etc. Since most active traders and investors are filing 1040 Schedule D for individual income tax, our guide is primarily based on that form’s layout and instructions. The other versions of Schedule D are typically identical or very similar.

BASIC LAYOUT OF THE IRS SCHEDULE D

The 1040 Schedule D form has three parts:

- Part I – Short-Term Capital Gains and Losses – Generally Assets Held One Year or Less

- Part II – Long-Term Capital Gains and Losses – Generally Assets Held More Than One Year

- Part III – Summary

The first two parts of the Schedule D are essentially identical when it comes to listing your trade activity for the current tax year. Lines 1 through 3 (Part I) and lines 8 through 10 (Part II) segregate amounts based on Form 8949 classifications: Box A, Box B, and Box C for short-term; Box D, Box E, and Box F for long-term. Those classifications will be explained later in this guide. Lines 1a and 8a allow a taxpayer to simply enter totals from their broker-provided 1099-B(s) for covered securities. However, this is only used if there are no adjustments required. Most active traders and investors do require adjustments to 1099-B reported amounts. We’ll explain why… Within each part there are four columns as shown below:

Additional lines on the Schedule D allow for the amounts which flow from various other forms, such as Form 6781 and Form 4797. Part III steps through summarizing the totals for use on the respective tax return.

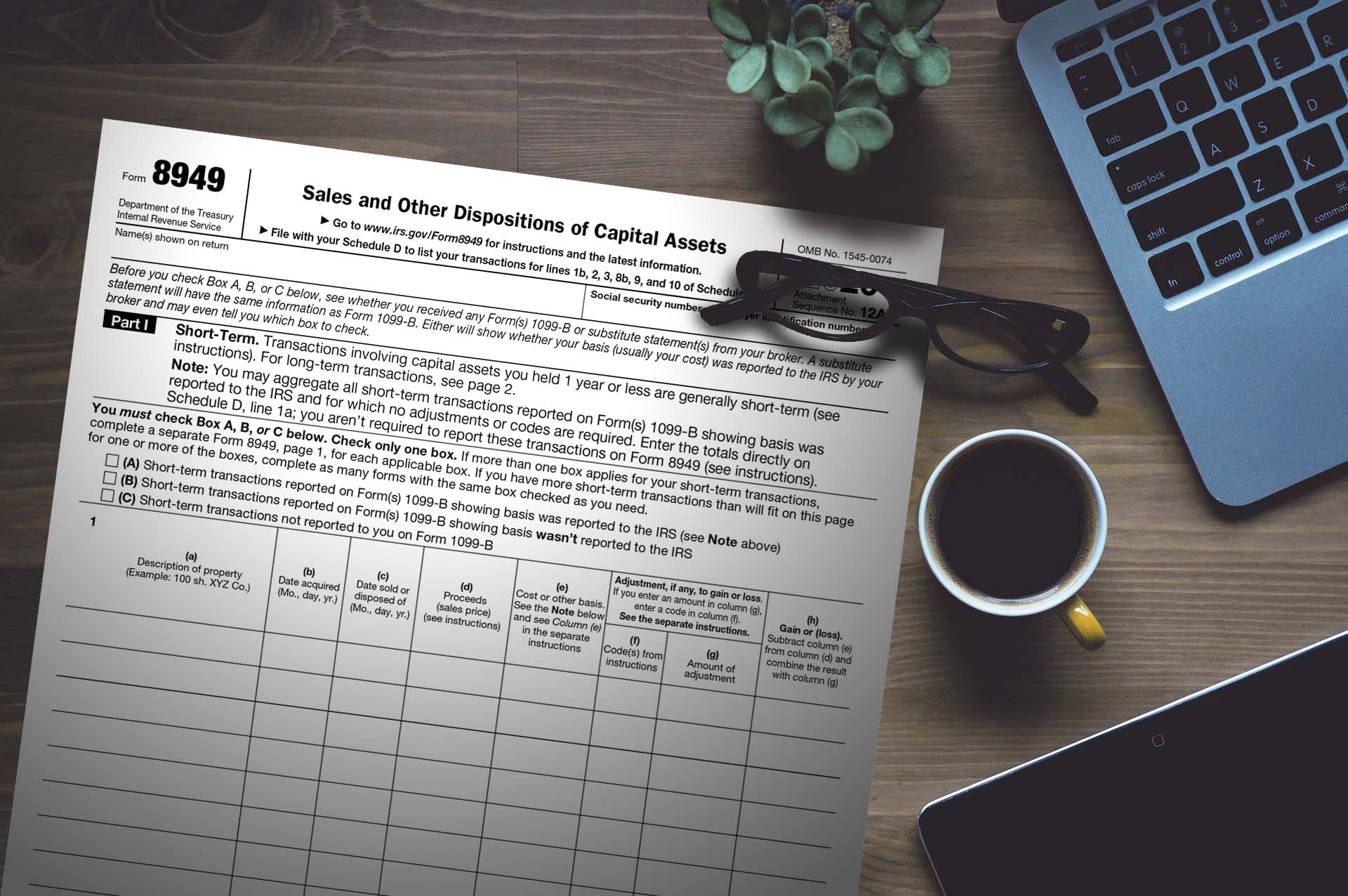

IRS FORM 8949 EXPLAINED

IRS Form 8949 is used by most traders and active investors to report the detailed trade history for capital gains and losses. Subtotals from Form 8949 are carried over to the Schedule D, discussed above.

Basic Layout of IRS Form 8949

The 1040 Form 8949 is laid out in two parts:

- Part I (1) – Short-Term

- Part II (2) – Long-Term

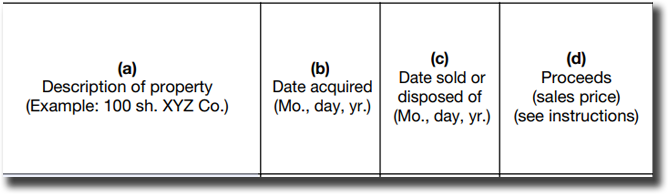

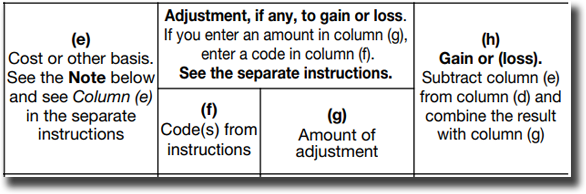

The holding period of the trade is generally what determines whether it is long or short term. Anything held one year (365 days) or less is considered short term, and anything held for more than one year (366 days or more) is considered long term. There are exceptions. For example, special wash sale rules can change a short term to a long term holding. Other tax rules may dictate the holding treatment regardless of the actual days held, such as with inherited stock. If in doubt, consult with a tax adviser regarding your situation. Each part of the form is almost identical when it comes to listing your trade activity for the tax year being filed. There are eight columns in each part as shown below:

Each part of IRS Form 8949 has three categories, indicated by the check box at the beginning of each section:

Part I

Part II

Because you may have transactions that fall into more than one of the above categories, for either part of the form, it is possible that you will have multiple Forms 8949 to file with your Schedule D. The next topic discusses the factors in determining which trades are reported in each category.

UNDERSTANDING IRS FORM 8949 CATEGORIES

It’s important to learn how a trade’s category is determined for Form 8949. Each part of IRS Form 8949 has three categories, A, B, and C for short-term transactions and D, E, and F for long-term transactions, as indicated by the check box at the beginning of each form.

Factors that determine which category a particular trade is reported under:

- Is the security reported on a Form 1099-B received from your broker?

- If YES – then the trade is reported in either category A/D or category B/E, the second factor will determine which category.

- If NO – then the trade is reported in category C/F.

- Is the security a ‘covered’ security, meaning that your broker is required to report cost basis information for the security? This should be indicated by box 6 on the 1099-B you receive.

- If YES – then the trade is reported in category A/D.

- If NO – then the trade is reported in category B/E.

What determines if a security is Covered?

The IRS has determined which securities are covered and non-covered. Basically, a covered security is one that the broker must report on the 1099-B and must report cost basis data for, by law. Non-covered securities may be reported on your 1099-B and may even have cost basis data reported, but they are still classified as non-covered because they are not required by the IRS. The IRS provides comprehensive instructions for brokers in determining covered versus noncovered. For more information about 1099-B reporting requirements, see the IRS instructions for 1099-B.

WHO NEEDS TO USE FORM 8949?

The IRS Instructions for Form 8949 state that it is used to report sales and exchanges of capital assets. Form 8949 is used by both individual taxpayers as well as corporations and partnerships. Form 8949 is used with the Schedule D for the return you file, including Forms 1040 and 1065, along with most other common tax return forms. See page 1 of the IRS Instructions for a complete list.

What is reported on Form 8949?

All sales and exchanges of capital assets are reported on Form 8949 according to the Form 8949 instructions. This includes stocks, bonds, equity options, and similar instruments. Sales are reported regardless of whether they were reported on a 1099-B by a broker.

Typically the following transactions are reported on the Form 8949:

- Stocks and Bonds

- Mutual Funds

- DRPs

- ETFs/ETNs

- Options

- Single Stock Futures (Securities Futures Contract)

Each transaction is reported on a separate row of the Form 8949. In general, individual traders and investors who file Form 1040 tax returns are required to provide a detailed list of each and every trade closed in the current tax year. Futures and Other Section 1256 Contracts are not reported on Form 8949. Regulated futures contracts are reported differently than most other securities on Form 1099-B and are typically not reported on Form 8949. Broad-based index options as well as contracts on many ETFs / ETNs qualify for Section 1256 treatment. Click here to learn more about Futures and Section 1256 Contracts.

Exceptions to Using Form 8949

Most active traders and investors report trading activity on Form 8949. The exception may be if you have filed for section 475(f) trader status. In addition, Section 1256 contracts as well as currency trading may not be reported on Form 8949. According to the latest IRS Form 8949 instructions, there are three additional exceptions / provisions which make filing a Form 8949 unnecessary:

- Exception 1. Reporting on Schedule D lines 1a, 8a: Exception 1 allows some taxpayers to report directly on Schedule D using lines 1a and/or 8a, however, there are three specific requirements that must all be met:

- You received a Form 1099-B (or substitute statement) reporting transactions in which the cost basis was reported to the IRS and there are no adjustments in box 1f (accrued market discount) or 1g (wash sale loss disallowed);

- AND, the Ordinary box in box 2 is not checked;

- AND, you don’t need to make any adjustments to the basis or type of gain/loss (short-term or long-term) reported;

- AND you are not electing to defer income due to an investment in a QOF (Qualified Opportunity Fund) and aren’t terminating deferral from an investment in a QOF.

If all of these requirements are met, then you may choose to report those transactions directly on Schedule D using lines 1a and/or 8a. However, this exception will rarely apply to traders and investors because typically they have nondeductible wash sale adjustments.

- Exception 2. Form 8949 Substitute Reporting: Rather than using the actual Form 8949, Exception 2 of the IRS instructions for Form 8949 allows taxpayers to attach a statement containing all of the same information as Form 8949 and in a similar format. Totals from the statement(s) are then entered on Form 8949. However, the detailed statements must still be sent to the IRS.

- Special Provision. For corporations, partnerships, securities dealers, and other qualified entities:Under this special provision, certain entities are no longer required to provide transaction details, but may simply enter summary totals on Form 8949 for a specific part(s). However, there are rules for this exception:

- You must file Form 1120S, 1065, or 1065-B, or be exempt from receiving Form 1099-B.

- You must have more than five transactions for the respective part of Form 8949;

If this exception benefits you, keep in mind that you are still required to maintain records of the details used to arrive at your totals, and these may be requested by the IRS. See the IRS Form 8949 Instructions for more details about these exceptions. IMPORTANT – Do not enter “Available upon request” unless specifically allowed based on Form 8949 instructions, as most traders and investors are required to report details of each transaction on Form 8949.

HOW TO COMPLETE FORM 8949

Form 8949 makes tax reporting of trades more complicated than ever for active traders and investors. Likely, congress had envisioned a simpler and more accurate reporting process when they passed cost basis reporting legislation. But the resulting IRS regulations are far from simple.

The Form 8949 instructions from the IRS rely on the concept that broker-provided 1099-B reporting contains the information needed for tax reporting. In theory, this concept is good, but in reality there are serious flaws and challenges. In polls conducted by TradeLog, 97% of active traders had circumstances that made the 1099-B incomplete for Form 8949 requirements.

Ideally, the IRS wants taxpayers to fill out Form 8949 with all of the information from the 1099-B, then correct that information if necessary and make additional adjustments not accounted for by the broker. In addition, any trades not reported on 1099-B would need to be accounted for. This can be an overwhelming task for active traders and investors with hundreds or thousands of trades, and often more than one trading account!

Software applications are very limited in handling Form 8949 in the IRS ideals. We have not found any software application that handles Form 8949 exactly as the IRS instructs. Some programs tout that they import 1099-B information from brokers. In those cases one must ask: How does that software verify that the 1099-B information is accurate and make needed corrections? How are additional wash sale adjustments made (those not required by the broker on 1099-B)? How are trades that are not reported on 1099-B (such as options) reported? Many popular tax software applications can be misleading and fail to provide the reporting needed for active traders and investors.

Remember, despite what a broker reports on Form 1099-B, you are still obligated to maintain and report accurate trade history records. Your broker is NOT required to provide you with IRS-ready tax reporting.

CHALLENGES WHEN COMPLETING FORM 8949

First In, First Out (FIFO)

If you do not specify a method, the IRS will assume you used the First In, First Out (FIFO) method. When using the FIFO method, the first shares purchased are considered the first shares redeemed. The oldest shares still available are considered the first ones sold. It takes quite a bit of work to go back and forth with each sale to find the correct purchase shares. Add to that the fact that you probably did not buy and sell an equal number of shares. Now your trade matching problem gets really complicated!

Reporting Short Sales on IRS Form 8949

Short sales are not reported the same as long trades. Basically, short sales get reported on IRS Form 8949 using the date that you closed or covered the short trade for both the Date Acquired and Date Sold. The Instructions for Form 8949 state (we italicized important parts):

Column (b)—Date Acquired Enter in this column the date you acquired the property. Enter the trade date for stocks and bonds you purchased on an exchange or over-the-counter market. For a short sale, enter the date you acquired the property delivered to the broker or lender to close the short sale. For property you previously elected to treat as having been sold and reacquired on January 1, 2001 (or January 2, 2001, for readily tradeable stock), enter the date of the deemed sale and reacquisition. Column (c)—Date Sold or Disposed Enter in this column the date you sold or disposed of the property. Use the trade date for stocks and bonds traded on an exchange or over-the-counter market. For a short sale, enter the date you delivered the property to the broker or lender to close the short sale.

Explanation for Date Acquired

“For a short sale, enter the date you acquired the property delivered to the broker or lender to close the short sale.” This is the trade date of the “buy to cover” transaction, rather than the date you sold the stock short.

Explanation for Date Sold

“For a short sale, enter the date you delivered the property to the broker or lender to close the short sale.” It may seem a little odd in that it seems to use the same date as the Date Acquired. However, the actual date that you delivered the stock to your broker is the settlement date, which is generally three business days after you closed the sale.

Section 1259—Constructive Sales Treatment for Appreciated Financial Positions

According to this rule, if the closing trade results in a gain, the Date Sold is reported as the trade date of the closing position. – See: IRS Revenue Ruling 2002-44 for details.

In summary:

- Date Acquired – Date Acquired is always the trade date for the short sale closing position.

- Date Sold – Closed at a Gain – If the short sale trade was closed at a gain, then the

- Date Sold is reported as the Trade Date of the closing position.

- Date Sold – Closed at a Loss – If the short sale trade was closed at a loss, then the Date Sold is reported as Settlement Date of the closing position. Short Sale Holding Period – Since the Date Sold is either less than one day from the Date Acquired in the case of a gain or three to five days from the Date Acquired in the case of a loss, short sales are always reported on Form 8949 as short-term, even if the buy to cover date was more than 365 days from the original short sale date.

PROBLEMS WITH IRS INSTRUCTIONS FOR FORM 8949

We have identified major problems with IRS instructions for Form 8949. Keep in mind, Publication 550 gives detailed rules for how capital gains and losses are calculated and wash sales adjusted. Form 8949 instructions suggest you do the following:

IRS Instructions: “If you receive Form 1099-B or 1099-S (or substitute statement), always report the proceeds (sales price) shown on that form (or statement) in column (d) of Form 8949. If Form 1099-B (or substitute statement) shows that the cost or other basis was reported to the IRS, always report the basis shown on that form (or statement) in column (e).” – 2020 Form 8949 instructions.

Problem: There is no consistent automated way to do this, so it must be done by manually entering each line. If you are an active trader that means likely thousands of entries! Some brokers and software applications tout that you can ‘import your 1099-B’, however, there is no standard and often the data is technically not the 1099-B reporting.

IRS Instructions: “If any correction or adjustment to these amounts is needed, make it in column (g).” – 2020 Form 8949 instructions. Later, the same instructions give multiple reasons why corrections or adjustments may be needed.

Problem one: To do this you will need a log of accurate cost basis data that you have kept (similar to what TradeLog records). Then you need to go line-by-line and compare what your broker reported on 1099-B, make adjustments and record on Form 8949 – a tedious task.

Problem two: Your broker adjusts the cost basis on Form 1099-B for wash sales, however, they only have to report wash sale adjustments between identical CUSIPS and in a single account. They are also allowed to group together buys into one lot which can limit adjusting wash sales for unequal buy/sell amounts. In contrast, you must adjust wash sales between stocks and options, and across all brokerage accounts – including IRAs. You must also match trades to account for unequal buys and sells in order to properly adjust wash sales. In other words, it’s possible that every single record on the 1099-B will be incorrect!

Problem three: The 1099-B does not typically provide details of the adjustments the broker has made to reported cost basis or sales proceeds. This makes verification of what the broker is reporting nearly impossible. How do you correct and adjust what cannot be verified in the first place?

Bottom Line: The IRS on the one hand says to use your Broker 1099-B to fill out Form 8949. However, they require traders to report gains and losses and wash sales in greater detail than brokers can ever report on the 1099-B. If you were to use the 1099-B data and then go back to verify and adjust, you would very likely have to make an adjustment to every line of the Form 8949. No software application can handle this automatically.

METHOD FOR REPORTING ACCURATE CAPITAL GAINS & LOSSES ON FORM 8949

Because of the flaws in Form 8949 requirements, and the overwhelming work involved in completing the 8949 in the IRS ideals, TradeLog utilizes a method for reporting accurate capital gains and losses based on the IRS requirements for taxpayers. Specific rules for traders and investors reporting investment income and expenses (including capital gains and losses) can be found in IRS Publication 550. Using this method, a Form 8949 can be generated with the software, and provide accurate tax reporting.

In order to fully comply with IRS tax reporting requirements as outlined in Publication 550, TradeLog uses the following process for entering trades on Form 8949:

- TradeLog keeps an accurate log of your actual trade history as reported by your broker. This includes: trade description, date of trade, type of trade, original cost basis or proceeds, commissions and fees – the 1099-B reporting does not contain all of this trade history.

- TradeLog matches trades by default as FIFO (with the ability to specifically match lots if needed) and then calculates gains and losses based on that matching.

- TradeLog also matches trades based on unequal buy/sell amounts according to wash sale rules – this is often not done on 1099-B reporting.

- TradeLog then adjusts for wash sales as outlined by Publication 550 – on unequal trades, across stocks and options, across all accounts. It then makes the necessary adjustments to gains and losses according to IRS rules – 1099-B reporting only makes limited wash sale adjustments and is not adjusted according to requirements for Form 8949 filing.

- TradeLog next classifies trades for reporting categories and completes Form 8949 lines, totaling each section to simplify completion of Schedule D.

For over a decade, TradeLog has been helping active traders and investors alike to better understand and report their capital gains on Schedule D. As IRS requirements for Form 8949 reporting continue to evolve, let TradeLog help you navigate the many challenges that generating accurate reporting requires.